By: Assistant Secretary for Economic Policy Ben Harris and Deputy Assistant Secretary for Macroeconomics Neil Mehrotra

The U.S. economic recovery from the Covid-19 pandemic has been remarkably fast, with the unemployment rate now near 50-year lows and real gross domestic product (GDP) growth of 5.7 percent in 2021. Job growth remains strong so far in 2022, with unemployment claims very low and a recent Fed survey showing dramatic improvement in household finances in 2021. However, the U.S. recovery may be substantially faster than commonly appreciated if growth is measured by gross domestic income (GDI).

The Bureau of Economic Analysis (BEA) maintains two distinct measures of aggregate economy activity: GDP and GDI. GDP measures expenditures on good and services provided to final users (households, government, etc.) while GDI measures aggregate income (wages, business profits, rental and interest income). Conceptually, these two measures are equivalent, but due to differences in the source data, these two series typically diverge. The BEA labels this divergence as statistical discrepancy, and, over the pandemic, the magnitude of the statistical discrepancy has grown significantly. A third measure, gross domestic output (GDO), is simply the average of GDP and GDI.

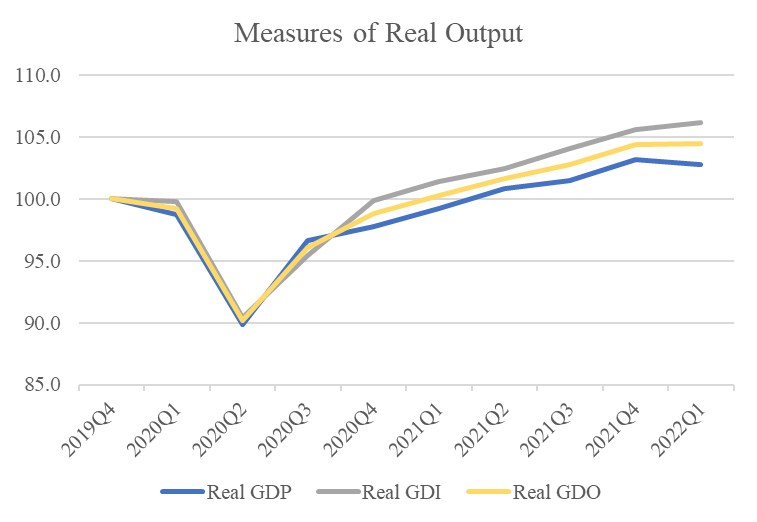

GDI has recovered significantly faster than GDP over the pandemic (see figure below), suggesting a stronger underlying recovery in economic output than GDP. This morning, with the release of GDI from the first quarter of 2022, the gap between GDI and GDP has grown to 3.5 percent—the largest on record. The divergence between GDP and GDI emerged in the fourth quarter of 2020; in that quarter, GDP grew at just 4.5 percent (annualized, as are all growth rates in this note) while GDI soared 19.6 percent. For the first quarter of 2022, today’s report showed that GDP contracted 1.5 percent, but GDI rose 2.1 percent.1

So, which of these three measures is more accurate for measuring economic output and the state of the recovery? This debate is not new. For example, the Council of Economic Advisers, in July 2015, released a report advocating the use of GDO as a preferred measure of economic growth, noting that GDO has historically “been a better gauge of the latest and presumably most accurate estimates of GDP growth than either GDP or GDI individually as well as a more stable predictor of future economic growth.”2

Conversely, some economists have argued that GDI is a better real-time indicator of the state of the economy.3 During the 2008 recession, for example, GDI deteriorated earlier and more quickly than GDP, suggesting a deeper recession. The first release of GDP showed a contraction of 3.8 percent in the fourth quarter of 2008; in the end, GDP was estimated to have contracted 8.5 percent in that quarter, more than double the original estimation. Importantly, revisions to both GDP and GDI brought estimates of the economic contraction in 2008 closer to what GDI was showing in real-time.

The faster observed recovery in GDI carries important implications for how one thinks about the overall recovery from the pandemic. First, GDI suggests more rapid recovery relative to GDP. In the current recovery, GDI shows economic output remarkably exceeding its pre-pandemic trend: based on today’s estimate of GDI for the first quarter of 2022, output is 1.2 percent above the level that would have been expected before the pandemic. By contrast, GDP suggests that output is still 2.0 percent below pre-pandemic trend. Put another way, GDI has grown at 2.7 percent over the pandemic – higher than the average output growth between 2015 and 2019, compared with GDP which has just grown 1.2 percent.

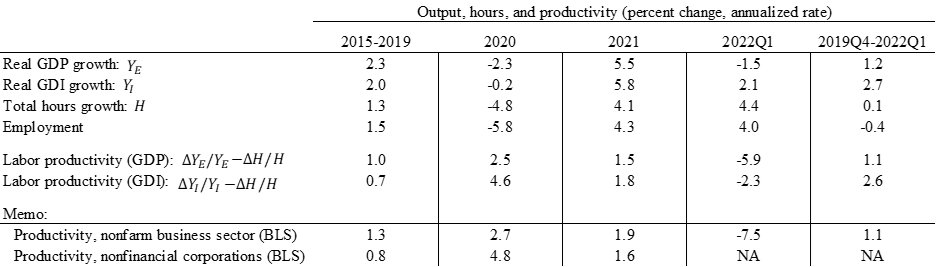

Second, the divergence between GDP and GDI carries implications for understanding trends in productivity — a key driver of wage growth and living standards over the medium term. The Bureau of Labor Statistics uses data on output, employment and hours to construct measures of labor productivity for various sectors of the US economy, and the key role of output implies that the measure employed — GDP or GDI — can have a consequential impact on the pace of productivity growth. If GDP is used to measure output, the combination of slow recovery in hours and below-trend GDP growth means that labor productivity has grown about 1.1 percent through the pandemic, roughly in line with pre-pandemic trend (see table below).

Meanwhile, GDI implies faster productivity growth through the pandemic. Through the lens of GDI, the above-trend output growth means that labor productivity growth is about 2.6 percent—nearly 2 percentage points higher than pre-pandemic trend. In other words, productivity growth appears to have accelerated during the pandemic if output is measured by GDI.

It remains to be seen whether such a productivity increase can be sustained as the pandemic wanes, but work from home, the reallocation of workers to higher productivity industries, the rise in labor mobility associated with a tight labor market, and strong business investment in equipment and software can be reasonably expected to boost productivity growth.4

Third, the gap between GDP and GDI has important fiscal implications. A stronger recovery in output means that the public debt burden is somewhat lower. Debt held by the public totaled $23.9 trillion as of the end of March. As a share of GDP, this ratio is 97.9 percent, but as a share of GDI, this ratio falls to 94.6 percent. From its peak in the second quarter of 2022, the publicly held debt-to-GDP has fallen 7.5 percent; for GDI, the analogous drop is 10.6 percent.

Treasury has seen a large increase in tax receipts relative to pre-pandemic levels, which also points to the strength of the underlying recovery. Through April, fiscal year corporate tax receipts totaled $216 billion, up 65 percent from the April average in 2017-2019, which is consistent with the strong rebound in corporate profits seen in GDI.5 The strong recovery has likely supported tax receipts from business income and capital gains that likely are also boosting individual income tax receipts. Through April, individual receipts totaled $1.72 trillion – up nearly 70% from 2017-2019 averages. Overall, strong receipts are likely to drive a record reduction in the budget deficit for FY 2022; the Congressional Budget Office now projects a record $1.7 trillion dollar reduction in the deficit for FY 2022.

In summary, the perception about the pace of the recovery depends critically on the metrics used to measure the macroeconomy. The BEA releases two measures of output, GDP and GDI, and there is good reason to consider either GDI or the average of the two measures when assessing the pace of economic growth. GDI will be revised, and it is possible that revisions will end up favoring GDP. However, GDI indicates an economy that is expanding at an especially rapid clip, has produced higher productivity growth, and has induced sharper declines in the debt burden.

[1] Initial GDP, GDI and GDO are indexed to 100 to abstract from the initial statistical discrepancy in 2019Q4.

[2] See Council of Economic Advisers (2015), “A Better Measure of Economic Growth: Gross Domestic Output (GDO),” Council of Economic Advisers Issue Brief.

[3] See Jeremy Nalewaik (2010), “The Income and Expenditure-Side Estimates of US Output Growth,” Brookings Papers on Economic Activity, pp. 71-106.

[4] The gap between productivity as inferred from GDP and GDI can be seen in BLS real output per hour for nonfinancial corporations. Productivity surged in 2020Q4 and remained high through 2021Q4 – the most recent data. Initial estimates of productivity for nonfinancial corporations will be available for 2022Q1 next week.

[5] Parsing underlying trends in corporate profit from the BEA data is complicated over the pandemic due to large pandemic-related transfers to businesses over this period with uncertain incidence.