By Assistant Secretary for Tax Policy Lily Batchelder and Deputy Assistant Secretary for Tax Analysis Greg Leiserson

Under his first executive order, President Biden directed agencies to examine their policies and programs to identify whether and how they perpetuate barriers to equal opportunity. Investigating structural barriers to opportunities for historically underserved communities is not just a moral priority for our country—it is critical to our economic success. But in order to tap into unrealized potential, we must first be transparent in analyzing the disparities that currently exist in our economy and in our country.

Given the increased reliance on the tax system as a means of delivering benefits in recent decades, it is critical that we understand how tax policies affect different families and whether policies implemented via the tax code are reaching all families. The IRS does not collect information on race and ethnicity on tax returns, so to facilitate analysis of disparities in tax policy, the Treasury Department has developed an approach to impute race and ethnicity in tax data, which it will continue to refine. Using this approach, the Department has conducted a first-of-its-kind analysis of the impact of tax expenditures on racial and ethnic disparities, which will increase transparency and improve our understanding of how existing tax policies work.

This analysis, the subject of a new Office of Tax Analysis (OTA) working paper, finds disparities in the benefits of some tax expenditures among White, Black, and Hispanic families. Tax expenditures are provisions of federal law that allow a special exclusion, exemption, or deduction from gross income or which provide a special credit, a preferential rate of tax, or a deferral of tax liability for certain activities. Examples include the preferential rates for capital gains, the home mortgage interest deduction, and the Earned Income Tax Credit. OTA working papers are works in progress intended to generate discussion and critical comment.

Researchers frequently analyze the distributional effects of tax policies across an array of demographic information, including income, family structure, age, and geography. However, it is challenging to perform such analysis by race and ethnicity because there is no single data source with both tax and race/ethnicity information. Tax liability does not depend on race or ethnicity, and this information is not collected on tax returns.

To overcome this challenge, Treasury researchers have developed a method to impute race and ethnicity in tax data. Under this method, researchers estimate the probability that the primary filer—the person listed first on the tax return—is Asian, Black, Hispanic, Native American, White, or multiple race based on other information available in the tax data. These probabilities are then used as weights to construct estimates for different groups.

A new OTA technical paper describes this method in more detail. OTA technical papers document the models, datasets, and methods developed by Treasury staff and used for policy analysis and estimates, and they are similarly intended to generate discussion and critical comment. Treasury staff continue to refine the imputation method, and the technical paper will be updated as the imputation method is refined.

The imputation method is an extension of a widely used method for imputing race and ethnicity known as Bayesian Improved First Name Surname Geocoding, or BIFSG. BIFSG and related methods have been used in a range of applications, perhaps most prominently in the study of disparities in health care and consumer finance.[1]

The new imputation method allows Treasury to conduct tax analysis by race and Hispanic origin for the first time, and the analysis of tax expenditures by race and Hispanic origin is the first analysis we have published using this capability. While there are many opportunities for additional research, this work is a critical step forward in Treasury’s work to advance equity analysis of tax policy.

Previous research on racial disparities in the tax code, such as research by law professors Beverly Moran, William Whitford, and Dorothy Brown, has used self-reported race data but did not have access to tax data.[2] This new work benefits from access to tax data and Treasury’s detailed tax models but relies on imputed, rather than actual, race and ethnicity information.[3]

Tax expenditures by race and Hispanic ethnicity

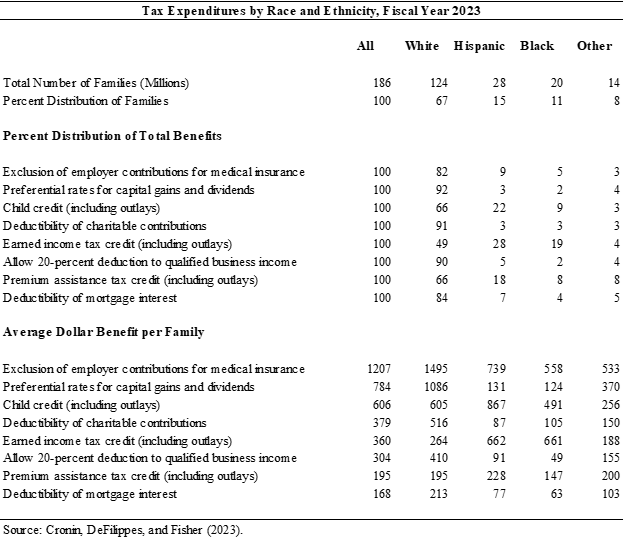

The new working paper on the distribution of tax expenditures, by Julie-Anne Cronin, Portia DeFilippes, and Robin Fisher of OTA, examines eight of the largest individual income tax expenditures. It estimates the distribution of benefits for certain racial and ethnic groups first on an overall per capita basis, and then within income deciles (tenths of the income distribution).

On an overall per capita basis, the paper finds that the preferential rates for capital gains and dividends, deduction for pass-through income, charitable deduction, home mortgage interest deduction, and deduction for employer-provided health insurance disproportionately benefit White families. In contrast, Black and Hispanic families, who make up a disproportionate share of low-wage workers, disproportionately benefit from the Earned Income Tax Credit, which is designed to help low- to moderate-income workers and their families. Hispanic families, who have comparatively low rates of employer-sponsored health insurance, also disproportionately benefit from the Premium Tax Credit, which provides assistance for the purchase of health insurance through the Marketplaces. Finally, Hispanic families disproportionately benefit from the Child Tax Credit. The current analysis focuses on Black, White, and Hispanic people due to high levels of uncertainty in estimates for other groups.

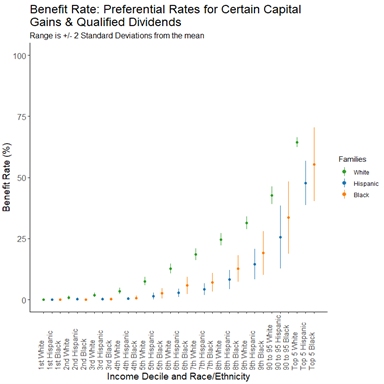

The analysis also examines disparities in the benefits of tax expenditures by race within income deciles. The findings within income decile are particularly stark for the preferential rates for capital gains and dividends. White families generally are more likely to benefit from these preferential rates across the income distribution (see figure below) and receive larger benefits at the high-income levels at which the benefits from these preferential rates are most pronounced. The same is likely true of the deduction for pass-through income, but the differences within income class are not statistically significant.

In contrast, the Child Tax Credit disproportionately benefits Hispanic families within income decile across the middle of the income distribution (but not at the top or bottom of the income distribution). The Earned Income Tax Credit disproportionately benefits Hispanic families in the lower-middle income ranges. The patterns within income deciles for these credits are more variable for Black families.

While the itemized deductions for charitable giving and home mortgage interest deduction disproportionately benefit White families overall, within income classes, they disproportionately benefit Black families in some upper-middle income ranges. Hispanic families also disproportionately benefit from the home mortgage interest deduction in some upper-middle income ranges.

This new research provides evidence of the disparities in the benefits of tax expenditures by race and ethnicity, but more work remains to be done to understand the reasons for these disparities and their implications. Differences in income, wealth, job characteristics, employer, family composition, access to credit, and so forth may give rise to these disparities in conjunction with the structure of the tax code, but more work is needed to determine which differences contribute the most.

To illustrate the challenges in interpretation, the relatively larger benefits from the deduction for home mortgage interest deduction for Black and Hispanic families in upper-middle income ranges could indicate that such families are less likely to have paid off their homes or pay higher interest rates on their mortgages, which could be indicators of disadvantage not advantage.

More work also remains to be done to improve the method to impute race and ethnicity information in the tax data used in this analysis.

While many questions remain, these initial findings emphasize the scrutiny that should be paid to existing and proposed tax expenditures that take the form of deductions, exclusions, and preferential rates. On a per capita basis, these types of benefits typically benefit a disproportionately White population and thus expand racial disparities. In contrast, refundable credits more frequently reduce racial disparities and can often be better designed to achieve the underlying policy goals as well.

[1] See, for example, Sorbero, Melony E., Roald Euller, Aaron Kofner, and Marc N. Elliott. 2022. Imputation of Race and Ethnicity in Health Insurance Marketplace Enrollment Data, 2015–2022 Open Enrollment Periods. The RAND Corporation.

[2] Moran, Beverly I., and William Whitford, 1996. “A Black Critique of the Internal Revenue Code.” Wisconsin Law Review 4, 751-820. Brown, Dorothy A., 2021. The Whiteness of Wealth: How the Tax System Impoverishes Black Americans—And How We Can Fix It. New York, NY: Crown Publishing Group.

[3] Taxpayer data used in the research was kept in a secured Treasury or IRS repository, and all results have been reviewed to ensure that no confidential information is disclosed.