Outreach

Across the country, the Homeowner Assistance Fund (HAF) Program Participants are identifying strategies to reach communities where residents were disproportionately affected by the COVID-19 pandemic.

As HAF progresses, Treasury encourages all Participants to evaluate their outreach strategies to ensure that all homeowners in need have the opportunity to access HAF funds. Participants have made great strides through the life of the program to partner with community stakeholders, bring awareness to the programs and provide access to HAF resources for those in need. In addition to financial assistance, HAF can also offer access to housing counseling and legal services. Effective outreach can help homeowners connect to services that can help prevent foreclosure and support housing stability.

The HAF Guidance (page 9) addresses promoting access to all eligible households:

Equity and Accessibility: HAF participants should design programs to be as accessible as possible to homeowners in different circumstances, including by offering multiple intake formats, and engaging with nonprofit organizations to provide additional pathways into the program.

Advantages to developing a comprehensive outreach strategy:

- Increases awareness of and access to the HAF program.

- Increased awareness and access results in decreased foreclosures and financial instability.

- Increased access to both financial assistance and housing stability services.

- Builds strong partnerships and networks that enable homeowner engagement and foreclosure prevention efforts.

- Builds long term infrastructure to provide comprehensive and homeowner-focused services.

Improving access to the HAF program is vital to ensuring that financial assistance is distributed those in need.

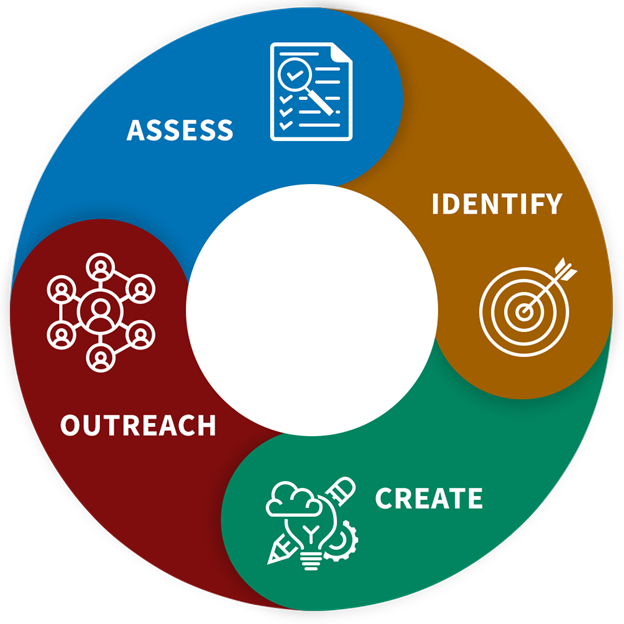

Steps to Take

- ASSESS geographic and cultural landscape of your community to determine needs

- IDENTIFY homeowners in financial distress

- CREATE strategy to provide housing stability services

- OUTREACH to identified targets according to your developed strategy.

Considerations

The following is a checklist to use as a guide in the evaluation of outreach strategy:

Assess

Have you completed a geographic analysis of where applications are coming from?

Why this is importantHigh need areas with little to no HAF participation may indicate lack of awareness of the program.

Identify

Have you identified trusted community based organizations?

Why this is importantCommunity based organizations often have a deep understanding of the community they serve and are trusted by residents. This may also apply to trusted organizations that work with homeowners and other key stakeholders.

Have you identified community partners that serve marginalized populations?

Why this is importantPartnerships are critical especially when working with the elderly, domestic violence and human trafficking survivors, and other marginalized communities.

Have you partnered with other state government departments, such as Human Services, that provide supportive services to homeowners?

Why this is importantOther state government departments will have access to a variety of different listservs and information. It's also an opportunity to combine financial resources and services.

Have you contacted homeowners associations?

Why this is importantEnables homeowner engagement and program visibility.

Create

Have you made your application accessible through multiple channels?

Why this is importantApplication accessibility accounts for those with or without technology capability – online, in person, and over the phone.

Have you developed a marketing strategy with a diverse portfolio of channels to advertise HAF?

Why this is importantA variety of advertisements i.e. social media, tv, radio, newspaper, mailed postcards, etc., will ensure you are promoting awareness to those harder to reach.

Outreach

Have you hosted events geared toward homeowners?

Why this is importantEnables homeowner engagement, promoting awareness of available resources.

Have you advertised in public places?

Why this is importantPosting flyers in public places frequented by homeowners, such as libraries and grocery stores, may reach those who cannot receive advertisements through radio, tv, or social media.

What's Next

Determine if your HAF Program has an established outreach strategy

- Are there ways to evaluate your strategy for equity and effectiveness?

- Are the right people, organizations, or community groups involved to execute your strategy?

Determine if a COVID-19 Pandemic Impact Questionnaire can be used in your HAF Program

- Determine who uses the questionnaire and how often it is used to evaluate and adjust your strategy.

- Are there specific factors that might impact how the considerations are executed?

- Are there other considerations that might bring increased success?

Examples of Partnerships

The State of New York has a multi-pronged approach to outreach to underserved populations. First, the HAF program contracted with community based organizations (CBOs) to promote outreach to key populations across different populations. Additionally, the state conducted virtual townhalls with elected officials to build awareness and worked with culturally competent housing counseling agencies to provide access to homeowners needing additional assistance. The State also hired a firm to conduct marketing campaigns and media buys to provide broader awareness building to the entire state to drive interest and uptake in HAF. To reduce barriers, the State used a 3rd party verification process to confirm eligibility, identity and income from the NY Department of Labor’s data. media ads focused in areas where distressed homeowners have historically experienced barriers to accessing assistance.

The State of Minnesota focused their outreach efforts for their HAF program on communities most impacted by housing instability such as Tribes, Black communities, communities with other people of color and people with disabilities. A significant component of Minnesota’s outreach includes engaging trusted community partners working for historically excluded and most impacted communities. Ten community-based organizations selected by Minnesota’s HAF program as HomeHelpMN Community Connectors had existing relationships with the identified communities and the ability to reach and build trust among potential eligible homeowners. The Community Connectors were able to propose events, strategies to get the word out about the HAF assistance, develop a workplan, and budget that was tailored to their organization and the communities they serve. Many Community Connectors employed door knocking and flyer campaigns to reach homeowners. The State of Minnesota supported these efforts by providing the content and printing services. Many Community Connectors relied on in-person events and workshops in each community to increase awareness and build trust among interested homeowners. Many of these organizations received federal funding for the first time through Minnesota’s HAF program as subrecipients. The State provided training and capacity building to their subrecipients to ensure compliance with federal requirements, including reporting, which in the future will support the capacity for the organizations to apply for and receive direct federal awards.

Examples of Data Driven Outreach

The State of Rhode Island assessed homeowner need based upon a set of six criteria: housing cost burden, concentration of non-white population, concentration of Hispanic population, foreclosure rate, homeowners earning less than $75,000 per year, and mortgage delinquency. The state reached out to homeowners in communities with the highest need by partnering with local community-based organizations, developing marketing resources, and deploying staff members to low-income and socially disadvantaged communities to assist homeowners, in particular people without access to or experience with the technology needed to apply for assistance.

The State of Tennessee has built into its HAF program capabilities to analyze the impact of HAF programs in real-time, allowing it to monitor the impact of HAF in high-need areas and adjust outreach strategies. As the program progresses, metrics will be reviewed to determine whether additional efforts are needed to reach and serve target populations.